International Equities: active vs multi-manager vs ‘smart-beta’ strategies

The featured chart plots the rolling 5-year excess returns and active risk (aka tracking error) outcomes of: (i) MSCI's factor [...]

The featured chart plots the rolling 5-year excess returns and active risk (aka tracking error) outcomes of: (i) MSCI's factor [...]

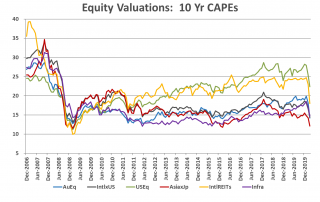

Further to our recent post on Sector Valuations which looked at the current & historical CAPE leveIs of MSCI equity [...]

The Accumulation chart decomposes the strategy's returns into: (1) market returns [yellow]; (2) factor returns [grey]; and (3) non-factor (alpha) [...]

Being primarily interested in longer term valuation metrics, the CAPE ratio applies real earnings per share (EPS) over a 10-year [...]

The relevance of active management The relevance of active management continues to be questioned, particularly under conditions awash with liquidity. [...]

Australian Equity Models: Managing Risk & Return Outcomes The chart looks at the risk & return outcomes of factor based [...]

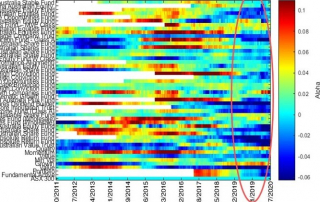

The charts show the average non-factor returns (commonly referred to as idiosyncratic returns or alpha) generated by our short-listed Australian [...]

Each quarter we update the equity valuations of the markets we invest in. Being primarily interested in longer term valuation [...]

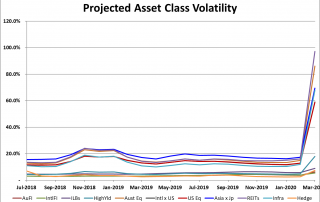

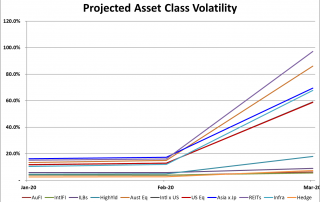

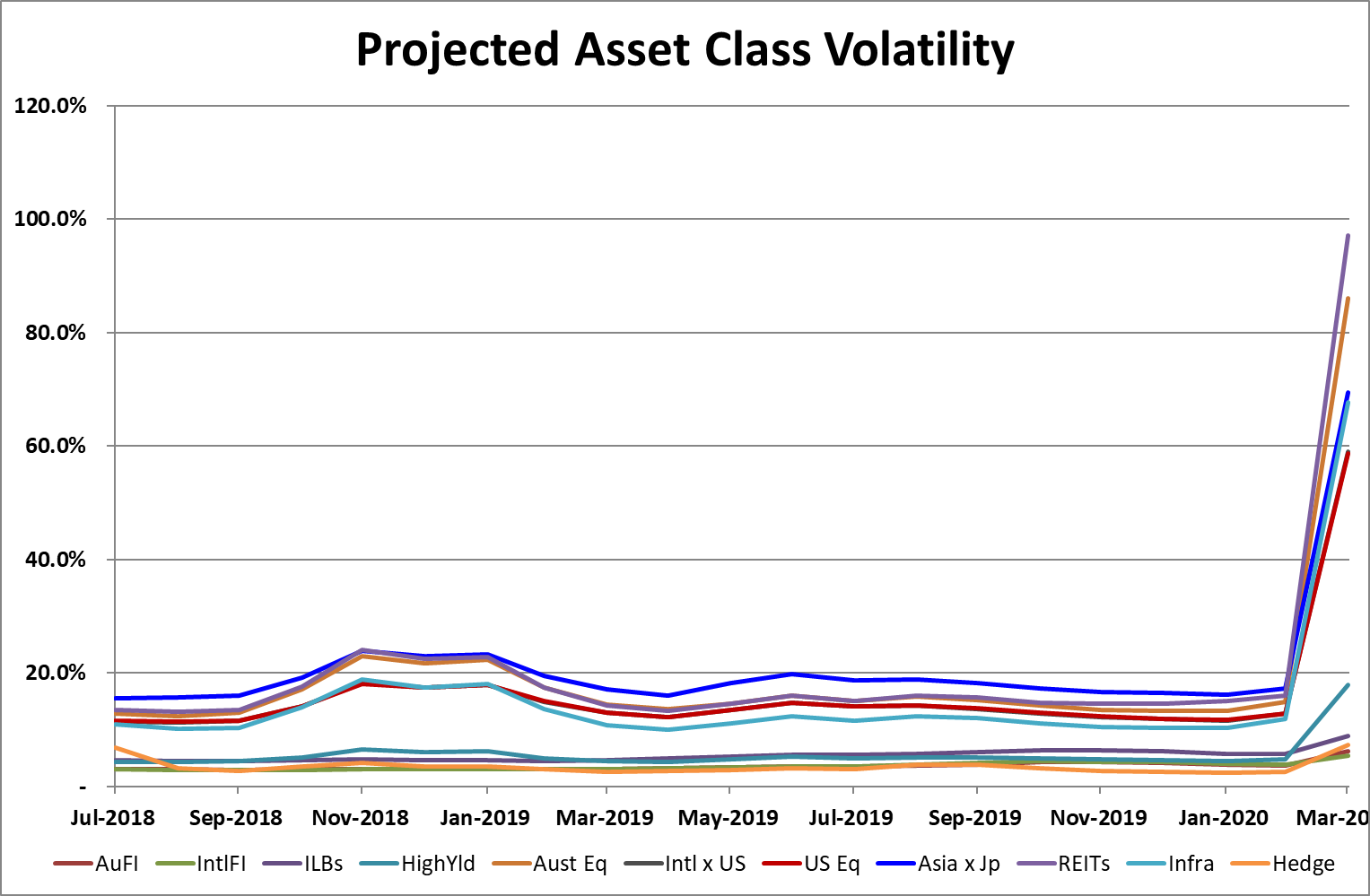

Each month, we monitor the risk levels of each sector we invest in, with the recent spike being nothing short [...]

The question for many investors is whether to hold their portfolios or to de-risk by selling into the recent rally. [...]

Summary Our 2019/2020 Australian Equity Review covered 153 strategies 101 strategies were screened out due to inconsistent and/or insufficient risk-adjusted [...]

{kind=link}

{kind=link}